Why Mission-Critical Operations Avoid Valuation-Inflated Partners

“Establish your foundation in discipline, perform your duty, and abandon attachment to success or failure.” — Bhagavad Gita (2:47)

In every cycle, those who anchor themselves in discipline and purpose endure. Markets reward narratives in the short run, but permanence belongs to those who build without attachment.

This is the 2nd Essay in a Three-part Series

- The Hidden Conflict Behind Outsourcing Decisions (this essay: labor-capital dynamics and governance discipline)

- Why Mission-Critical Operations Avoid Valuation-Inflated Partners (vendor financial stability)

- From Arbitrage to Governance: Twenty-Five Years of Fully-Loaded Cost, Workforce Stability, and the Changing Economics of Labor (25-year cost analysis and convergence)

Analytical Framework: This analysis is grounded in financial mathematics and cycle-tested evidence. It is not written in the language of identity, politics, or sentiment, because mission-critical operations cannot be safeguarded by narratives alone. Numbers reveal what narratives conceal: survival odds, compounding discipline, and the enduring difference between speculation and foundations. The frameworks presented here emerge from decades of operational experience across multiple economic cycles, informed by direct observation of how markets reward sustainable business models while systematically repricing speculative structures.

Disclaimer: This analysis contains forward-looking statements and market observations for informational purposes only. It is not intended as investment advice or securities recommendations. Market conditions and company performance can vary significantly from historical patterns and projections discussed herein. References to economic policies or regulatory environments are factual observations rather than political commentary.

Executive Summary

- Markets rewarded narratives; cycles re-price toward cash generation and operational fundamentals

- Speculation vs. Foundations: speculation builds thin, binary structures; foundations build permanence across cycles

- 70% early-stage failure odds make many vendors unsuitable for mission-critical business processes

- Procurement blind spot: features, price, and compliance checked; survival probability systematically ignored

- Operational risk transfers to clients when vendor fragility is concealed through growth narratives

- BPO fundamentals: 20-25% EBITDA margins, 80%+ cash conversion, recession-tested demand, scale economics advantages

- Pricing contrast: SaaS 8-12% annual increases vs. BPO 3-5% tracking costs, yielding 30-40% lower TCO over multi-year periods

- Strategic imperative: choose foundation-built partners; avoid binary-outcome vendors for critical operations

Strategic Analysis

Why Mission-Critical Operations Avoid Valuation-Inflated Partners

“In every market cycle, capital flows disproportionately toward sectors that capture imagination while systematically undervaluing those that generate cash. Understanding this pattern—and positioning accordingly—represents perhaps the most compelling asymmetric opportunity in today's market environment.”

Executive Premise

This analysis examines a fundamental market disconnect: while sophisticated private capital systematically acquires profitable outsourcing operations at premium multiples, public markets continue discounting the same sector that has demonstrated resilience across multiple economic cycles.

The investigation reveals why valuation inflation creates operational instability and how mission-critical business functions require financially sustainable partnerships for competitive advantage.

Part I: The Vendor Risk Business Leaders Underestimate

Speculation vs. Foundations

When you're managing payroll for hundreds of employees, processing customer orders that drive quarterly results, or maintaining compliance systems that ensure regulatory standing, you cannot build your operations around companies designed for binary outcomes.

Every economic cycle exposes the fundamental difference between businesses built on speculation and those built on enduring foundations. Speculation reshapes priorities, rewarding speed over discipline, appearance over substance, and headlines over durability. Companies governed by speculation optimize for the next funding round, the next valuation milestone, the next acquisition discussion—not for the next decade of operational survival.

This difference begins at the foundation level. Structures built on speculation assume continuous external support, hiring faster than internal economics can sustain and constructing operations around expectations of future funding rather than present discipline.

Speculation disguises itself through carefully constructed language. Runway becomes the polite way of saying we will run out of money. Pivot becomes the euphemism for our foundation was unsound. Growth capital becomes the sanitized term for survival funding.

By contrast, businesses built on enduring foundations—positive cash flow, disciplined growth, conservative commitments—survive and strengthen through economic cycles.

The Hidden Mathematics of Vendor Selection

Studies of companies raising early-stage capital (seed and Series A) consistently show that more than 70 percent never reach sustainable profitability or long-term operational stability.

Traditional procurement frameworks reinforce this problem by measuring price, features, and compliance while ignoring survival probability. The most fundamental question—what is this business truly built on?—remains unasked. Enterprises unknowingly build payroll systems, compliance operations, and customer processes on structures whose very survival depends on continued speculation.

When economic cycles contract, speculation breaks in predictable patterns: workforce reductions that degrade service capabilities, strategic shifts that abandon core client functions, desperate acquisitions that terminate partnerships without adequate transition periods.

Most business due diligence processes focus extensively on cybersecurity, technical capabilities, and compliance while treating vendor financial stability as secondary consideration. This approach systematically underestimates the operational risk that follows from vendor financial distress, regardless of company size.

The operational impact of vendor financial distress follows predictable patterns across company types:

- Mass layoffs at vendors disrupt customer support that middle market companies depend on for operational assistance

- Strategic pivots abandon specialized features that portfolio companies had built dependencies around

- Fire-sale acquisitions terminate services with minimal transition periods for critical business processes

- Leadership turnover creates constant contract renegotiation during operational dependencies

- Desperate cost-cutting degrades service levels that businesses built operational assumptions around

Private equity portfolio companies often demonstrate more sophisticated vendor risk assessment than their public counterparts. When managing defined holding periods and specific return targets, vendor instability that threatens operational continuity becomes unacceptable.

The Financial Sustainability Assessment

The assessment framework examines vendor stability through financial mathematics rather than growth narratives:

Critical risk indicators include:

- Companies valued at 15x+ annual revenue requiring impossible growth trajectories to justify investor returns

- Consistent quarterly losses despite substantial revenue growth indicating unsustainable unit economics

- Annual price increases exceeding 8% driven by investor return pressure rather than operational cost inflation

- Heavy dependence on external funding for operational continuity creating acquisition pressure

Sustainability indicators for operational continuity:

- Positive operating cash flow demonstrating viable business model independent of external funding

- EBITDA margins above 15% indicating structural profitability rather than revenue growth subsidization

- Diversified client base across industries reducing single-point-of-failure risk for vendor survival

- Multi-year contract visibility enabling precise cash flow modeling and operational predictability

Board Checklist: Vendor Financial Sustainability

- Foundation: Is this business cash-flow positive today?

- Survival odds: What is the probability this vendor exists through the life of our contract?

- Valuation pressure: Are price increases driven by cost inflation or investor return targets?

- Concentration: How concentrated is the vendor's revenue by client or sector?

- Contract visibility: What multi-year visibility does the vendor have into its own cash flows?

- Knowledge retention: How is institutional knowledge retained across economic cycles?

Part II: Historical Pattern Analysis - The Software Collapse & AI Trajectory

The last cycle has already tested these foundations—here is what happened when speculation met a contraction.

The Predictable Pattern of Valuation-Driven Instability

The median high-growth software company experienced 75-90% valuation decline from peak as markets recognized the mathematical impossibility of sustaining growth-at-all-costs business models. Companies that raised at 20x+ revenue multiples required impossible growth trajectories to justify investor returns, creating internal pressures incompatible with stable enterprise partnerships.

Enterprise Operational Impact During Market Corrections

The software sector collapse demonstrated how vendor financial distress creates operational disruption across companies of all sizes. When high-growth software companies faced systematic repricing, the enterprise impact extended far beyond stock prices:

Predictable operational disruption patterns:

- Vendor workforce reductions degraded customer support and product development capabilities

- Strategic pivots abandoned specialized features that businesses had integrated into operations

- Acquisition activity terminated services with limited transition periods for dependent operations

- Executive turnover created contract uncertainty during critical operational dependencies

- Cost reduction initiatives degraded service levels that companies had built operational assumptions around

The mathematics were unforgiving for venture-funded vendors: Companies that raised at 20x+ revenue multiples required impossible growth trajectories to justify investor returns, creating internal pressures incompatible with stable enterprise partnerships.

The AI Sector: Following the Same Script at Larger Scale

The AI sector trajectory follows identical mathematics at unprecedented scale: Foundation model companies command valuations exceeding major banks despite minimal demonstrated revenue, while unit economics present even greater challenges than software predecessors.

Compute costs scale exponentially with model sophistication while talent expenses represent 60-80% of operating costs. Infrastructure spending requires constant capital infusion while competition from technology giants creates subsidized competitive pressure that makes sustainable pricing impossible.

Enterprise leaders selecting AI vendors based on demonstration capabilities rather than business model sustainability are repeating the fundamental error that created widespread operational disruption during the software correction.

Our Approach: Innovation Through Risk Management

We respect and support technological innovation and forward progress. The transformative potential of artificial intelligence is undeniable, and enterprises that fail to capture these capabilities will face competitive disadvantage. However, we believe strongly in managing the substantial risks around these innovations.

Many highly innovative AI companies have broken capitalization tables and inflated valuations that create fundamental structural problems difficult to recover from. When a foundation model company raises at $5 billion valuation with $50 million revenue, the mathematical requirements for investor returns create internal pressures incompatible with enterprise partnership stability:

Broken cap table recovery is nearly impossible because:

- Down-round financing destroys employee equity incentives and triggers talent exodus

- Investor liquidation preferences make sustainable business model pivots economically unviable for founders

- Acquisition requirements force strategic decisions based on acquirer value rather than client operational needs

- Operational cost structures optimized for growth-at-all-costs cannot adjust to profitability requirements

Our strategic AI integration approach eliminates these risks:

Rather than exposing clients to vendor dependency, we serve as the stable integration partner that captures AI's transformative benefits while eliminating vendor risk through proven methodologies:

- Technology abstraction layers enable us to integrate best-of-breed AI capabilities from multiple providers without creating single-vendor dependencies that could disrupt enterprise operations.

- Vendor diversification strategies across AI platforms ensure that capability advancement continues regardless of individual vendor financial stability, acquisition outcomes, or strategic pivots.

- Implementation discipline prioritizes demonstrable operational improvements over technological novelty, ensuring AI deployment strengthens rather than threatens business continuity.

- Human-in-the-loop methodologies leverage AI for efficiency gains while maintaining operational control and quality assurance that mission-critical processes require.

This approach enables clients to capture cutting-edge AI capabilities through our proven infrastructure without building operational dependencies around vendors designed for binary outcomes. Innovation advances through risk management rather than despite it.

Part III: The Business Process Outsourcing Alternative & Market Evidence

The software collapse demonstrated the operational chaos that follows vendor financial distress, while AI companies follow identical trajectory at larger scale. This environment highlights the strategic value of partnerships with financially sustainable providers that have demonstrated operational continuity across multiple economic cycles.

Sustainable Economics from Inception

Contrast with business process outsourcing fundamentals:

- Sustainable unit economics from inception — 20-25% EBITDA margins, 8-15% annual growth, no venture capital required

- Recession-tested business models — Sector expanded during 2008-2009 while software companies laid off millions

- Predictable cash generation — 80%+ EBITDA conversion, demonstrated across thousands of companies over decades

- Minimal failure rate — Geographic diversification, contract diversification, and positive cash flow create natural stability

Scale and durability evidence: Global BPO market exceeds $300+ billion annually with India's IT services exports alone at $200+ billion, growing steadily for 20+ years with leading firms operating profitably across multiple decades.

The scale economics advantage: Unlike artificial intelligence and software vendors where costs increase exponentially with complexity, business process outsourcing achieves superior unit economics through scale. Shared infrastructure, process expertise, and operational knowledge compound rather than degrade profitability as operations expand. This fundamental difference enables sustainable pricing structures that venture-funded competitors cannot replicate without achieving positive cash flow first.

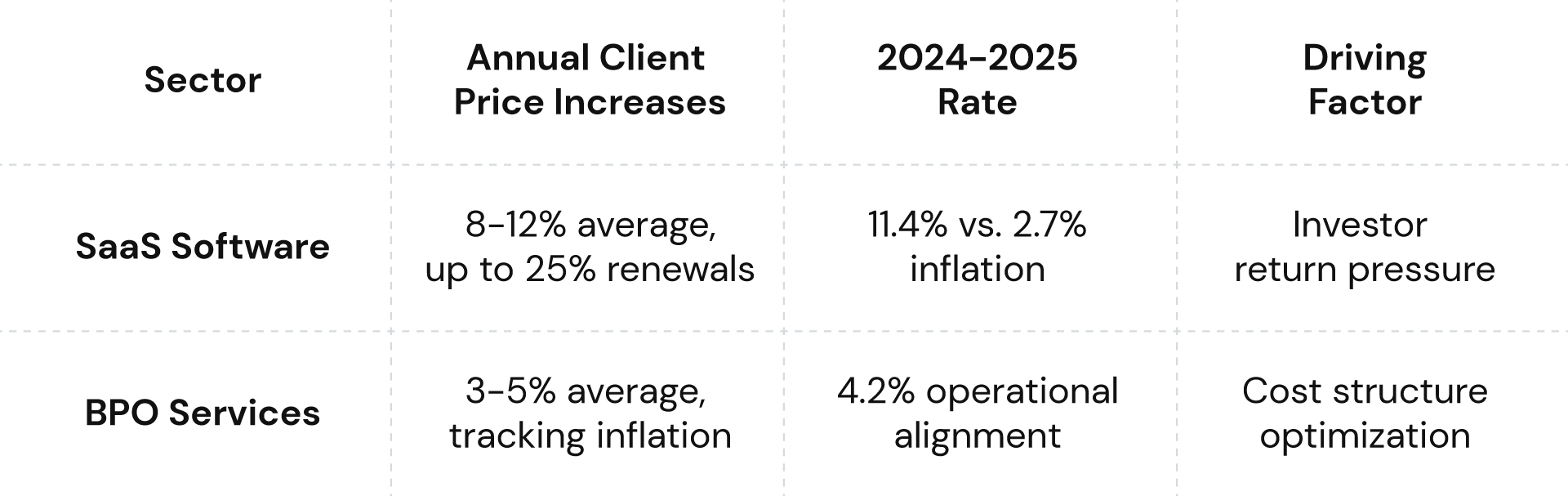

The Pricing Predictability Advantage

Valuation-inflated vendors face relentless pressure to justify multiples through aggressive pricing increases. Software and AI companies must generate revenue growth matching investor expectations—often requiring 15-25% annual increases to maintain valuation support.

The data reveals stark operational contrast:

SaaS inflation analysis:

- 73% of SaaS vendors implemented price increases in 2024, with major providers locking customers into 7% annual escalations

- Price increases run 5x higher than G7 market inflation, creating systematic cost pressure for enterprise budgets

- Switching cost exploitation allows vendors to implement aggressive increases once integration dependencies develop

BPO pricing discipline:

- Established providers maintain pricing discipline at less than half the SaaS rate, tied to operational cost inflation rather than investor return requirements

- Geographic arbitrage benefits enable capability expansion without corresponding price increases

Total cost reality: Factoring switching costs, implementation disruption, and pricing volatility, financially stable providers deliver 30-40% lower total cost of ownership over multi-year periods.

Currency structural advantages create additional value: USD appreciation versus emerging market currencies generates natural cost deflation that established providers pass to clients rather than extracting for margin expansion. This currency hedging effect helps enterprises manage operational costs during inflationary periods while providing geographic economic diversification.

Scale economics favor established providers: Unlike AI vendors where compute costs increase exponentially with scale, BPO operations achieve better unit economics through scale advantages. Network effects, shared infrastructure, and operational expertise compound rather than degrade profitability, enabling sustainable pricing that venture-funded competitors cannot match.

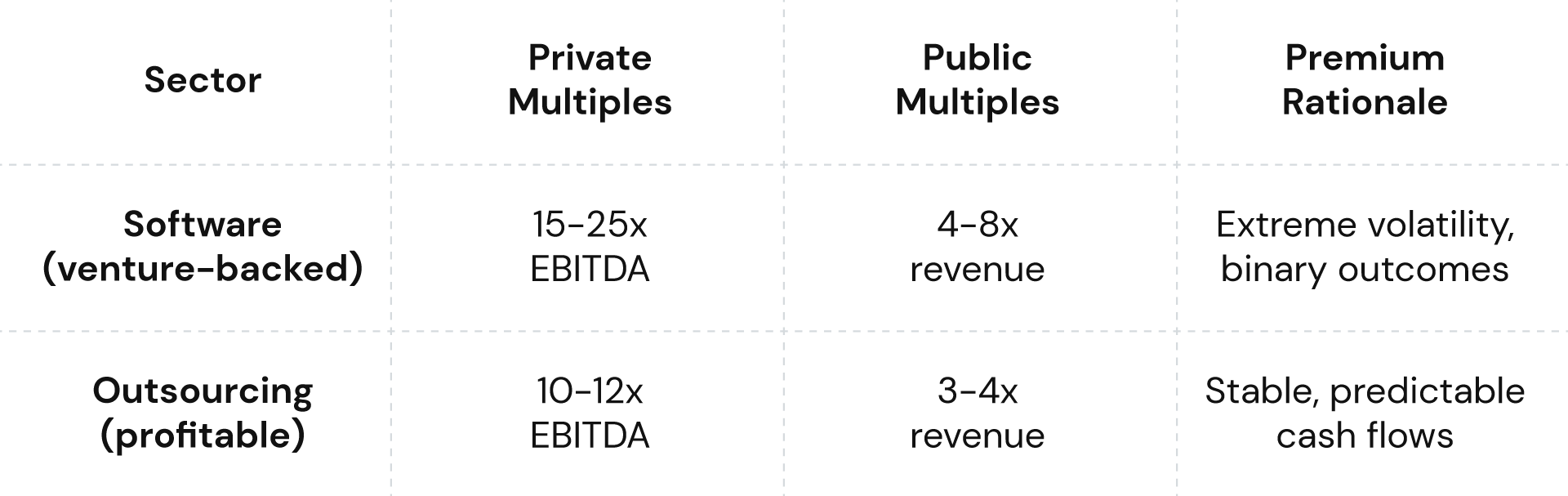

Market Evidence: Private vs. Public Valuation Disconnect

2025 transactions demonstrate sophisticated capital recognition:

- 60,000+ FTE global BPO provider acquired at $1.6+ billion by institutional capital

- 1,400+ FTE nearshore specialist acquired by PE-backed professional services firms

- Multiple mid-market transactions at 10-12x EBITDA premiums while public Indian IT services companies trade at 3-4x revenue discounts

Private equity consistently pays premiums for operational stability:

Why sophisticated allocators prefer outsourcing investments:

- Contract visibility enables precise cash flow modeling with 80%+ accuracy over 3-5 year periods

- Geographic diversification mitigates single-market risk while providing currency hedging benefits

- Recession-resistant demand provides downside protection as enterprises optimize costs during downturns

- Proven scalability requires no venture capital dependency, eliminating funding risk from investment thesis

Part IV: The Perils of Leverage

A significant factor in our sector's perceived commoditization stems from leverage. Companies carrying substantial debt cannot afford to act independently or think across cycles. Their behavior becomes dictated not by long-term client partnership, but by immediate demands of lenders and sponsors.

Leverage forces a common playbook: reduce costs to protect margins, consolidate delivery centers to satisfy efficiency ratios, and impose annual price increases to cover debt service. Service brands that might otherwise differentiate themselves begin to look and sound interchangeable, because they are all bound by the same financial constraints.

For clients, the risks are pronounced. During economic contraction, leveraged providers must prioritize covenant compliance over client commitments. Workforce reductions, service degradation, and abrupt strategic shifts become necessities imposed by capital structure rather than management choice. The result is operational instability for enterprises that believed they were purchasing continuity.

Independence from leverage changes the foundation entirely. A provider that is self-financed, profitable, and liquid can prioritize permanence over short-term financial engineering. It can invest in client relationships, talent, and infrastructure with confidence that comes from not being forced into homogenized behavior. Financial independence represents not merely a balance sheet position, but a strategic advantage that compounds across cycles.

Part V: Our Strategic Positioning & Market Cycle Advantage

Financial Independence as Operational Insurance

We've structured our business specifically as operational insurance for enterprises that cannot afford vendor risk within mission-critical processes. This positioning becomes increasingly valuable as market corrections separate sustainable business models from venture-subsidized experiments.

Profitable since inception eliminates external funding dependency that creates vendor instability and acquisition pressure. Our pricing remains stable independent of capital market conditions or investor return requirements, enabling long-term budget predictability for enterprise partners.

Geographic diversification across multiple cost-advantaged markets provides natural hedging against currency fluctuation, political instability, and single-market economic disruption while maintaining service delivery consistency across economic cycles.

Client diversification across industries and economic cycles creates recession-resistant revenue stability. When technology companies reduce spending during corrections, financial services and healthcare maintain operational requirements, providing natural portfolio balance.

Talent and institutional knowledge retention represents a critical but underappreciated advantage. When venture-funded vendors experience financial distress, institutional knowledge walks out the door with departing employees. Training investments, process documentation, and client-specific expertise disappear during talent exodus. Established providers maintain knowledge bases and institutional memory across market cycles, protecting enterprise investments in vendor relationships and operational integration.

Partnership scale dynamics solve the enterprise vendor paradox: Many venture-funded vendors are too small for enterprises to represent priority relationships, yet become too integral to enterprise operations to lose without disruption. This creates the "too small to matter, too big to fail" problem that leaves enterprises vulnerable during vendor distress. Established providers are properly sized for enterprise relationships—large enough for meaningful partnerships, stable enough for long-term commitments.

Technology Integration Without Vendor Risk

Our approach to AI and automation represents sophisticated innovation management: We capture technological advancement through established infrastructure while eliminating the vendor dependency risks that threaten enterprise operational continuity.

Technology abstraction layers enable best-of-breed AI integration across multiple providers without creating single-vendor dependencies. When individual AI vendors face financial distress or acquisition, our clients maintain capability continuity through diversified implementation strategies.

Human-in-the-loop methodologies leverage artificial intelligence for efficiency and capability enhancement while maintaining operational control that mission-critical processes require. This approach delivers superior outcomes compared to fully automated systems that lack oversight and quality assurance.

Implementation discipline prioritizes demonstrable operational improvements over technological novelty. AI deployment strengthens business continuity rather than threatening it through experimental vendor relationships or unproven technology dependencies.

The result: clients capture cutting-edge capabilities through proven infrastructure without accepting the vendor financial risk that follows from building operations around companies optimized for acquisition rather than operational excellence.

Market Cycle Recognition Creates Asymmetric Advantage

Historical pattern analysis reveals consistent technology cycles:

Technology hype phases create valuation inflation based on transformation promises rather than demonstrated unit economics. Venture capital temporarily subsidizes unsustainable operations until funding contractions expose mathematical impossibility. Market corrections systematically favor cash-generating businesses over growth-without-profits models.

Current market position analysis: We are in the late stages of AI valuation inflation with early indicators of inevitable correction. Enterprise leaders who recognize this pattern and position accordingly gain significant competitive advantages through strategic vendor selection.

Long-term competitive advantage compounds through market awareness:

Operational excellence strengthens through deepening client relationships that cannot be replicated through capital infusion or technology demonstrations. Financial discipline enables strategic flexibility during corrections, allowing capability investment when competitors face existential pressures.

Market position improves during downturns as consistency and reliability become premium values when competitors experience operational disruption from funding constraints or acquisition pressure.

The Strategic Assessment Framework

Enterprise leaders require assessment criteria that prioritize business model sustainability over transformation promises. The framework examines vendor financial health through multiple dimensions while recognizing that mission-critical operations demand partners capable of long-term operational continuity independent of acquisition outcomes or funding cycles.

Strategic Conclusions

The Fundamental Choice for Business Leaders

Valuation inflation systematically undermines business model sustainability, creating operational risk that mission-critical business functions cannot absorb. The software collapse provided clear demonstration of this pattern, while AI companies follow identical trajectory at larger scale with greater potential for operational disruption.

Mission-critical operations cannot afford to build around vendors designed for binary outcomes. The switching costs, operational disruption, and business continuity risks are too severe for enterprise and middle-market companies operating in competitive environments.

Strategic vendor selection represents competitive advantage that compounds over time. Enterprises that recognize financial sustainability as operational necessity position themselves advantageously relative to competitors accepting vendor risk within critical business processes.

Market Dynamics and Positioning

Market corrections consistently favor operational fundamentals over growth promises and transformation narratives. Every technology cycle concludes with capital flowing toward cash-generating businesses while growth-without-profits models face systematic repricing.

Partnership orientation enables sustainable differentiation through long-term relationships with financially stable providers that create operational capabilities compounding over time while competitors manage vendor transition disruption.

The convergence of elevated interest rates, extended investment holding periods, and systematic repricing of unsustainable business models has created an environment where operational stability commands premium recognition from sophisticated allocators.

The Strategic Imperative

For enterprises operating mission-critical functions, this represents both opportunity and imperative: strategic vendor selection based on financial sustainability rather than technological novelty creates enduring competitive advantage while protecting against operational disruption that inevitably follows vendor financial distress.

No board would accept 70% failure odds in any other operational domain—yet many accept them unknowingly in vendor selection by partnering with speculation-driven companies rather than foundation-built providers.

The choice for business leaders is fundamental: Build operational capabilities around partners designed for longevity, or accept increasing risk within business processes that cannot afford interruption.

While technological promises dominate headlines and capture imagination, operational reliability compounds quietly but decisively across market cycles. In a world where vendor financial distress has become common, strategic vendor selection represents perhaps the most important—and underappreciated—competitive advantage available to enterprise leaders.

For operations that cannot afford disruption, financial stability isn't optional—it's the foundation of reliable partnership.

Speculation is temporary. Foundations endure.

About Assivo

Assivo is an execution partner specializing in structured delivery across operations, finance, and data workflows. We build managed teams that run seamlessly and consistently—so leaders can focus on growth, not supervision.